Home Mortgage Disclosure Act

HMDA Auditing, Outsourcing and Consulting Services

We help covered mortgage lenders efficiently achieve their HMDA compliance goals.

ADI brings more than 20 years of experience and expertise to your team to help assess your HMDA compliance needs, implement sound and comprehensive HMDA procedures, and evaluate the accuracy of your annual and/or quarterly LAR filings.

Our HMDA consulting services include customized HMDA audits, compliance program assessment, policies and procedures advisement, and HMDA program management.

The accuracy and completeness of HMDA data is critical to fair and responsible lending risk management, as well as lending distribution analysis for both Fair Lending and Community Reinvestment Act (CRA) compliance. HMDA data integrity is an essential component of effective compliance management for these programs. ADI provides differing levels of data quality assistance, depending on your circumstance.

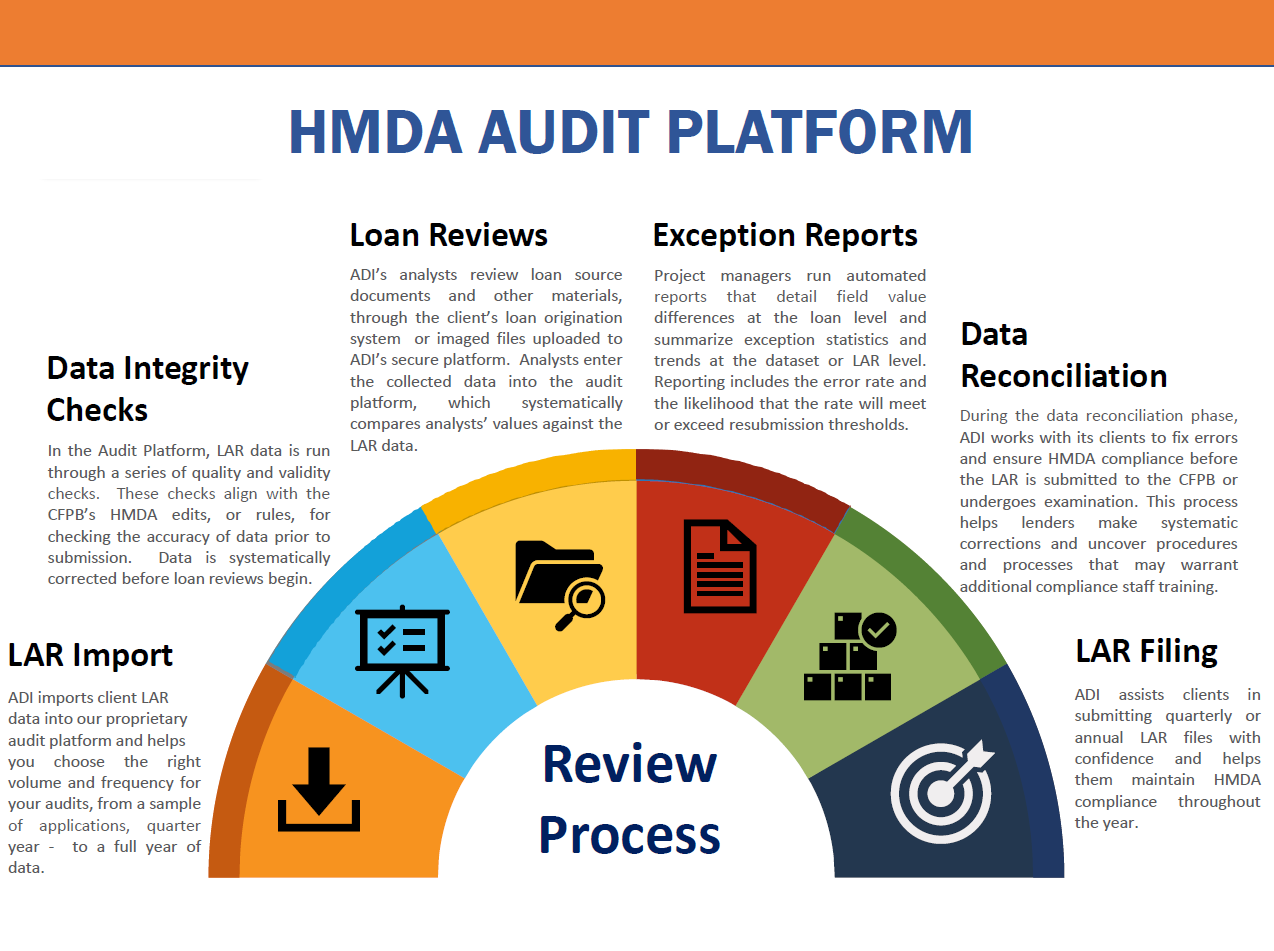

To streamline the HMDA LAR testing process, ADI has developed a proprietary testing software platform. We use an online secure environment that houses our turn-key HMDA audit solution. Experienced and knowledgeable staff use the web-based platform to complete a HMDA audit from start to finish. All work is conducted remotely and results are delivered and discussed promptly to ensure your company reports HMDA LARs accurately and in a timely manner.

Examiners first determine whether institutions have the compliance framework in place to promote accurate collection and reporting of HMDA data. ADI helps lenders assess their current HMDA program or design a system from the ground up. From there, we work with you to implement a plan that will grow with your institution, maintain relevance, and adapt to new regulations and reporting requirements.

Substantial new reporting requirements went into effect for data collected in 2019. Your institution’s policies and procedures must stay current with these changes in regulations and updates to your business processes, and information systems. ADI works with you to establish a new program or upgrade your existing HMDA policy and procedures, based on your needs. We design the policy or enhancements your compliance program requires, and we work with you to implement them.

Keeping your entire team up to date and in line with your institution’s practices, as outlined in policy and procedures, requires regular training. ADI offers fully customizable training based on the programs you offer and the challenges specific to your LAR reporting. ADI’s training program, Building HMDA Skills, provides guidance and instruction using real-world scenarios and interactive problem-solving to help every staff member, from the loan officer to the Chief Compliance Officer, “get it right.”

Demonstrating compliance and having confidence in your internal operations is crucial to your institution’s success. When outsourcing compliance work it’s important to work with advisors who understand your industry. If your institution does not have an in-house HMDA compliance program, parts or all of the program can be outsourced to ADI. In this partnership, our consultants schedule periodic check-ins, perform transaction testing, and provide ongoing advisement and training.

We will design and implement the right solution to meet your HMDA compliance needs.

Recent Engagements

Need a proposal?

We look forward to proposing the right solution that meets your needs.

Download our HMDA Services Brochure to learn more...

Enter your contact information below to download ADI's HMDA Services Brochure.