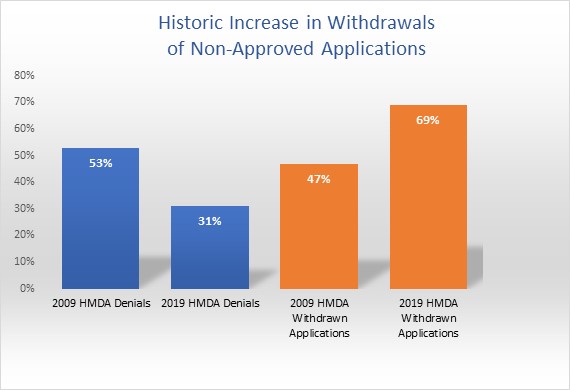

Withdrawn applications reflect an increasing proportion of non-approved first-lien mortgage applications as denials have become relatively less numerous. A decade ago, based on 2009 HMDA data, denials comprised just over one-half of non-approved first-lien applications. Denials fell to less than one-third of non-approvals a decade later. Over the same timeframe, withdrawn applications increased from under one-half to over two-thirds of non-approvals.

As withdrawals become more numerous, understanding the reason(s) for these consumer decisions plays an increasingly important role in identifying potential Fair Lending risk. In ADI’s recent article, we pose and offer an answer to the question: What are the possible reasons for a withdrawal and how can these reasons be used to inform Fair Lending modeling design?