The September release of the 2014 data submitted under the Home Mortgage Disclosure Act (HMDA) has several uses. In this article, we discuss the utility of these data in evaluating your institution’s exposure to HMDA compliance risk related to two data categories: government monitoring information and action type coding. By benchmarking your organization’s performance against your peers in these areas, you can identify whether your operational processes related to these categories signals HMDA compliance risk that requires immediate attention.

How Well Are You Reporting Government Monitoring Information?

One aspect of HMDA compliance that the publicly available data can provide insight on is the frequency of reporting government monitoring information (GMI). This category of data represents the recording of race, ethnicity and gender of each applicant and co-applicant. Applicants may voluntarily provide this information with their applications, however, if they do not, in some circumstances, lenders are required to make an effort to supply the missing data based on available resources. For example, if a loan officer is in a face-to-face meeting with an applicant and the applicant decides not to self-report their GMI, then visual observation can be used to determine these data points.

One aspect of HMDA compliance that the publicly available data can provide insight on is the frequency of reporting government monitoring information (GMI). This category of data represents the recording of race, ethnicity and gender of each applicant and co-applicant. Applicants may voluntarily provide this information with their applications, however, if they do not, in some circumstances, lenders are required to make an effort to supply the missing data based on available resources. For example, if a loan officer is in a face-to-face meeting with an applicant and the applicant decides not to self-report their GMI, then visual observation can be used to determine these data points.

Lenders are not expected to record GMI on every application. There are a number of cases in which a lender may be incapable of recording this information, such as on applications received via the Internet or over the phone that were ultimately withdrawn. Yet the 2014 HMDA data show that many lenders are substantially less likely to report GMI than their peers, as seen in the chart below. While differences in business models may explain some of the differences in the patterns, ADI’s experience with clients indicates that operational issues often drive the failure to report GMI.

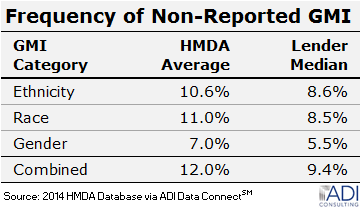

In 2014, 12.0 percent of originations reported under HMDA did not include GMI from at least one of the three GMI categories available in the public data. From a lender perspective, the median frequency of non-reported GMI among all HMDA reporters for any of the three GMI categories was 9.4 percent.

In 2014, 12.0 percent of originations reported under HMDA did not include GMI from at least one of the three GMI categories available in the public data. From a lender perspective, the median frequency of non-reported GMI among all HMDA reporters for any of the three GMI categories was 9.4 percent.

These numbers serve as useful benchmarks to measure your organization’s performance in complying with HMDA requirements for reporting GMI. Lenders that are near or below these levels likely have lower HMDA compliance risk related to GMI reporting. However, for lenders that have non-reported GMI frequencies that are substantially greater than these levels, their HMDA compliance risk may be greater.

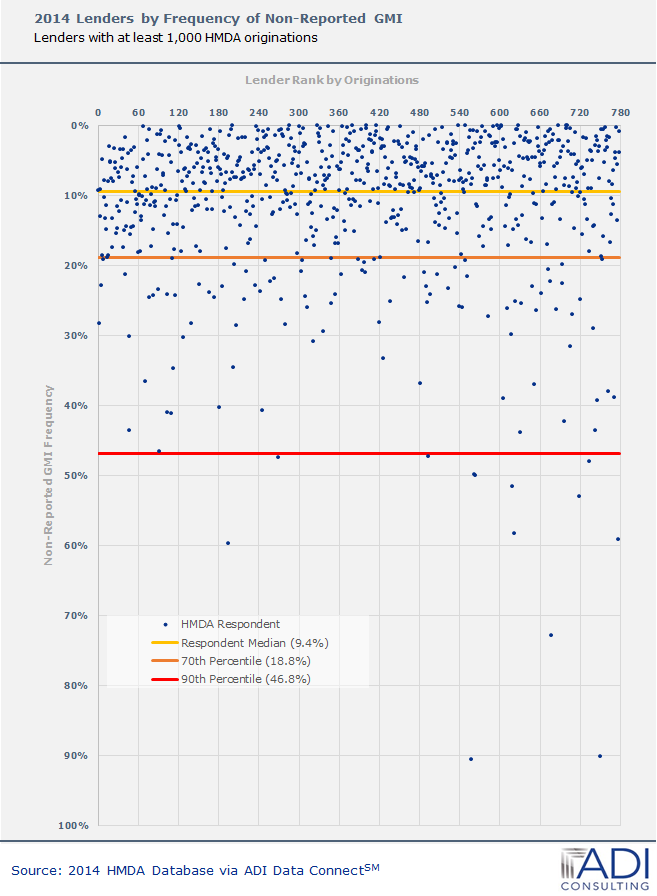

The adjacent chart represents the frequency of non-reported GMI on 2014 HMDA originations for the 779 lenders that originated at least 1,000 loans in 2014. The data show that 107 lenders, or 13.7 percent, had a non-reported GMI frequency at or above the 70th percentile level of 18.8 percent. These lenders likely face higher exposure to HMDA compliance risk than those performing equal to or better than the median level of 9.4 percent.

Government agencies, examiners, community organizations and other users of HMDA data rely on GMI to identify Fair Lending compliance violations. If users are unable to draw meaningful conclusions about your organization’s Fair Lending risk due to a high frequency of non-reported GMI, then examiners may flag your HMDA data and investigate why your organization performs worse than your peers in reporting GMI. Such scrutiny can lead to considerable compliance costs, including monetary penalties for identified HMDA violations to the dedication of resources to scrub, correct and re-submit HMDA data.

In addition to the direct compliance costs associated with HMDA, a high frequency of non-reported GMI will have implications on the evaluation of your Fair Lending compliance. Examiners may decide to use a proxy to guess the GMI attribution in order to try and draw meaningful conclusions about Fair Lending. Since this is an estimation methodology, there is a chance that you will be assessed with a higher level of Fair Lending risk than if self-reported or if observational information was recorded during the application or subsequent HMDA review process. Increased Fair Lending risk may result in another layer of compliance effort and additional costs.

Is Your Organization Accurately Coding Action Type?

The 2014 HMDA data also reveals insight into lenders’ processes for assigning action codes to applications. More specifically, the 2014 HMDA data may inspire questions regarding how your organization classifies applications as one of the three non-approval action codes: denied, withdrawn by the applicant, or closed for incompleteness.

The 2014 HMDA data also reveals insight into lenders’ processes for assigning action codes to applications. More specifically, the 2014 HMDA data may inspire questions regarding how your organization classifies applications as one of the three non-approval action codes: denied, withdrawn by the applicant, or closed for incompleteness.

Assigning the correct non-approval action code can present difficulties for many HMDA reporters. In our experience with clients, it is not uncommon, during a review of loan files, to see denied applications miscoded as withdrawn or to see withdrawn applications miscoded as closed for incompleteness. There are several reasons for these occurrences, such as insufficient policies, poor training and lack of documentation related to the application disposition decision.

As we discussed above for insufficient reporting of GMI, errors in recording the correct action type can lead to significant HMDA compliance risk exposure. As the adjacent chart shows, there may be substantial differences in how your organization codes action types compared to your peers. While these differences may be due to differences in organizational strategy, substantial discrepancies from similarly situated peers raise important questions regarding best practice procedures during the application process and the recording of HMDA data. High or unusual rates of any specific action type may lead examiners to scrutinize the processes for recording HMDA data. In addition to its effect on HMDA compliance risk, inaccurate action type coding can complicate Fair Lending underwriting analyses, which only adds to overall compliance risk exposure.

As we discussed above for insufficient reporting of GMI, errors in recording the correct action type can lead to significant HMDA compliance risk exposure. As the adjacent chart shows, there may be substantial differences in how your organization codes action types compared to your peers. While these differences may be due to differences in organizational strategy, substantial discrepancies from similarly situated peers raise important questions regarding best practice procedures during the application process and the recording of HMDA data. High or unusual rates of any specific action type may lead examiners to scrutinize the processes for recording HMDA data. In addition to its effect on HMDA compliance risk, inaccurate action type coding can complicate Fair Lending underwriting analyses, which only adds to overall compliance risk exposure.

According to the 2014 HMDA data, 64.4 percent and 35.6 percent of applications were approved and not-approved, respectively. These are benchmarks that we consider when reviewing a lender’s HMDA data. Since action types are critical to Fair Lending underwriting analyses, substantial differences from these benchmark levels may lead to research into how application action types are coded. Lenders with a relatively high frequency of withdrawn or closed for incompleteness applications versus denied applications may signal a systemic problem of miscoding denied applications as one of the other non-approval action types. Similarly, cases in which a lender has a relatively high frequency of closed for incompleteness versus withdrawn applications will raise questions about the lender’s policies and execution in assigning these codes correctly.

In general, when we observe patterns in action type coding that are substantially different from what we expect to see, we will conduct research to gain confidence in the processes for coding action type. Given the implications and associated costs that these errors can have with regard to your HMDA compliance, we recommend that you become aware of your organization’s patterns compared to your peers.

Being Proactive and Confident in Your HMDA Reporting

In summary, the 2014 HMDA data is a useful tool that can help you identify potential HMDA compliance issues that require your attention. Peer benchmarking of your GMI reporting performance and action type coding distribution is a proactive method that can aid in ensuring that your organization’s HMDA reporting processes are effective or in need of improvement. Peer benchmarking these and other HMDA data points, is an important piece of your HMDA compliance processes, that can minimize scrutiny from examiners and prepare you to address any questions that may arise regarding your HMDA compliance in reporting GMI and action type data.

About the Author

Jonathon Neil

Jonathon is a Senior Consultant for ADI with expertise in Fair Lending compliance, CRA compliance, data mining, and geographic information systems. You can contact Jonathon at jneil@adiconsulting.com or 703.665.3707.